What Is Next For Multifamily Transactions?

What Happened. The Federal Reserve began a cycle of interest rate hikes in Q1 2022 to stem the tide of inflation. Since then, SOFR has spiked approximately 500 bps and the 10-year Treasury has increased 225 bps, with the consequence that:

The average cap rate on multifamily real estate (MFR) transactions have widened almost 100 bps to 5.7%;

The quarterly dollar volume of MFR transactions in Q1 2024 plummeted to $21.2B from $73.1B in Q1 2022.

We believe transaction volume plummeted because (i) borrowing costs greater than cap rates created ‘negative leverage’ that drove prospective MFR buyers out of the market and (ii) sharply lower MFR property valuations caused prospective sellers to defer liquidity exits for as long as possible.

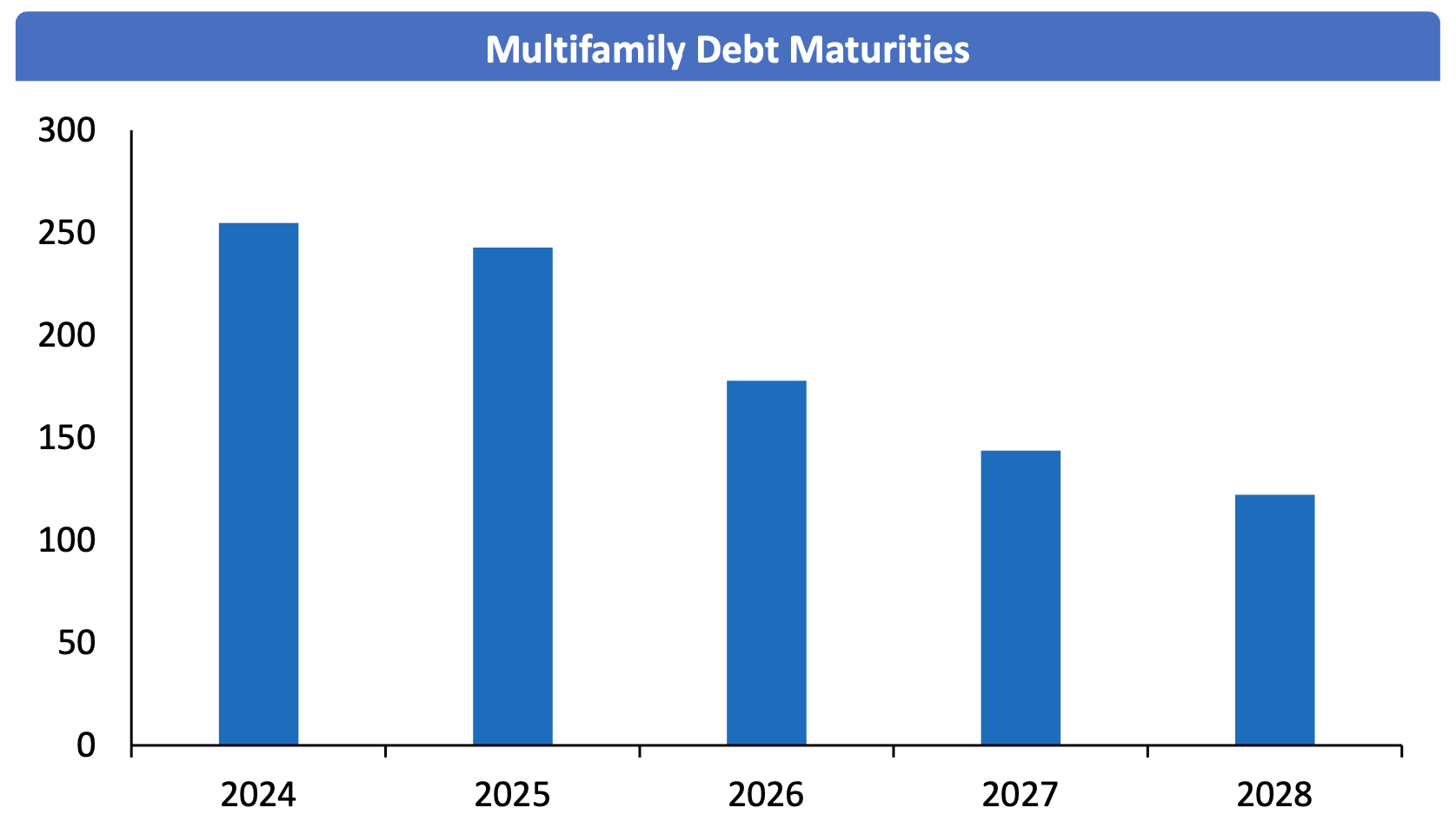

Liquidity Cannot be Deferred Indefinitely. During the 2020-2022 period, when new construction of MFR increased and transaction volumes were high, developers and acquirors took advantage of SOFR rates at ~25 bps and funded their projects and acquisitions with 75-80+% advance rate, three-to-five year floating rate debt. These loans are now maturing in significant volumes but, with SOFR now at more than 5%, these loans cannot be refinanced in the amount of the outstanding debt because loan-to-value and fixed charge coverage ratio covenants are not achievable without a significant equity capital infusion.

What’s Next. Prospect believes that the pending maturities of MFR mortgage debt is creating a window over the coming 12-24 months where current owners, after exhausting lenders’ patience with forbearance extensions, will be forced to recapitalize or sell MFR properties in order to avoid foreclosure. We expect to see prospective MFR buyers that have liquidity begin to jump into the market to provide the liquidity that these ‘unwilling sellers’ require to avoid foreclosure, albeit at prices that reflect price capitulation reflective of what we see as becoming a distinctly buyers’ market.

Disclosures

Not an Offer or Solicitation: This is for informational purposes only and is not an offer or solicitation to purchase or sell any financial instrument or service to any person in any jurisdiction. This is not intended to be construed as investment advice, an investment recommendation, investment research, or a recommendation about the suitability or appropriateness of any security, commodity, investment, or particular investment strategy. Reliance upon this information is at the sole discretion of the listener and the listener should consider the investment objectives, risks, charges, and expenses of any investment carefully before making it. This is intended to be shared as National Property REIT Corp. (“NPRC” or "We") brand awareness and illustrate NPRC’s role in owning and operating real estate in the market segments discussed herein.

Unless otherwise mentioned, the views, opinions and/or beliefs contained herein are those of NPRC employees. Other past or present NPRC employees, or other past or present employees of NPRC’s affiliates, may not necessarily share the same views, opinions and/or beliefs of present NPRC employees, and may not make, or may not have made, the same decisions regarding the ownership, operation and financing of real estate in the market segments discussed in herein. These views, opinions, beliefs, estimates and projections are made in relation to the facts known at the time of preparation and are subject to change at any time without notice. DO NOT RELY ON ANY OPINIONS, BELIEFS, PREDICTIONS OR FORWARD-LOOKING STATEMENTS CONTAINED HEREIN. Certain statements made throughout this information may be “forward-looking” in nature. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. There can be no assurance that any trends discussed during this presentation will continue and neither NPRC nor any of its affiliates has any responsibility to update this presentation to account for such changes. Certain information contained herein may have been obtained from third party sources. Although NPRC believes such sources to be reliable, NPRC makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties.

A number of factors may prevent each of NPRC’s properties from generating sufficient net cash flow or may adversely affect their value, or both. These factors include, but are not limited to, national economic conditions, regional and local economic conditions (which may be adversely impacted by plant closings, business layoffs, industry slow-downs, weather conditions, natural disasters, and other factors), local real estate conditions (such as over-supply of or insufficient demand), changing demographics, perceptions by prospective tenants of the convenience, services, safety, and attractiveness of a property, the ability of property managers to provide capable management and adequate maintenance, the quality of a property’s construction and design, increases in costs of maintenance, insurance, and operations (including energy costs and real estate taxes), changes in applicable laws or regulations (including tax laws, zoning laws, or building codes), potential environmental and other legal liabilities, the level of financing used by NPRC in respect of its properties, increases in interest rate levels on such financings and the risk that NPRC will default on such financings, each of which increases the risk of loss, the availability and cost of refinancing, the ability to find suitable tenants for a property and to replace any departing tenants with new tenants, potential instability, default or bankruptcy of tenants in the properties owned by NPRC, potential limited number of prospective buyers interested in purchasing a property that NPRC wishes to sell, and the relative illiquidity of real estate investments in general, which may make it difficult to sell a property at an attractive price or within a reasonable time frame.

The distribution of this information is restricted by law. No action has been or will be taken by NPRC to permit the possession or distribution of this information in any jurisdiction, where action for that purpose may be required. Accordingly, this information may not be used in any jurisdiction except under circumstances that will result in compliance with all applicable laws and regulations.