Not All Multifamily Real Estate is Created Equal

Introduction

From 2019 to present, U.S. commercial real estate has undergone dramatic transformations in both use and investment. The onset of the coronavirus pandemic curtailed employment in various job categories and forced the adoption of remote and hybrid work structures, accelerating migration trends to suburban communities away from urban centers. The Federal Reserve (“Fed”) and government responded to these exogenous disruptions with accommodative interest rate policies, direct consumer support packages, as well as fiscal stimulus and infrastructure spending.

We believe cheap, plentiful financing and drastic undersupply in fast-growing markets catalyzed an unprecedented wave of investment in multifamily real estate, particularly new development in markets that were experiencing waves of new residents.

As with most market cycles where the economy is benefiting from substantial stimulus policies, inflation spiked and market conditions quickly inverted. The Fed responded to historic inflation with sharp increases to interest rates while previously under-served markets now have a glut of new multifamily supply.

Many investors view the recent market reversals as a cautionary tale applicable to the whole of commercial real estate, multifamily included. NPRC believes those participants miss the trees for the forest. The value of quality multifamily assets with strong fundamentals is, in our opinion, being overshadowed by a fear of (i) higher rates for longer as inflation persists above The Fed’s 2.0% target, (ii) moderating to negative rent growth, (iii) the peak in supply and (iv) whether the economy will remain strong or backslide into a recession in 2025.

Herein, we discuss the fact that not all multifamily real estate is created equal when it comes to issues relating to future rent growth, exposure to over-supply, and the impact of high interest rates and government policy on the U.S. economy. And, in this regard, we focus on where in the multifamily sector market fundamentals remain compelling—namely, the naturally-affordable workforce housing segment of the overall market that caters to families with annual incomes in the range of $40,000 to $70,000 and are renters by necessity because they are unable to afford owning a single-family home.

Surge in Transaction Volume

Multifamily investment surged in 2021 and 2022 following the onset of the COVID-19 pandemic. Apartment transaction volume peaked in 2021 at $358.4 billion – nearly 100% higher than the prior peak of $195.1 million in 2019. With the increase in dollar-volume coupled with an increase in the number of properties trading, valuations spiked with average per-unit prices increasing 35% to $233K in 2022 from $173K in 2019 (10% compounded annualized growth rate or “CAGR”).

Source: Real Capital Analytics (as of 1Q 2024)

Source: Real Capital Analytics (as of 1Q 2024)

This spree of investment reflected the demand shift from changes in consumer preferences with a pandemic-inspired prevalence for remote and hybrid work, urban migration to suburbs in low-cost states, and the ensuing increase in household formation. This demand shift resulted in a spike in average multifamily rents and cap rate-compressed valuations fueled by buyers’ underwriting their proformas assuming continued outsized rent growth.

Source: Yardi, Real Capital Analytics (as of Q1 2024)

The Bad Interest Rate Bet

Throughout 2019 to 2022, an estimated $87B of multifamily loans were originated with 3-year terms and floating interest rates(1) with loan-to-value (“LTV”) ratios reaching 75% or higher. The acquisition thesis underlying these deals was the anticipation of recapitalizing the underlying property with long-term, fixed-rate debt after executing the business plan the acquiror intended to execute during the first three years post-closing of the subject acquisition. The assumption to recapitalize and withdraw equity was predicated on the Fed continuing a zero, or near zero, interest-rate policy.

Unfortunately, interest rates did not stand still: in March 2022, the Fed made its first rate hike and has since followed with 10 more which caused interest rates to soar and, in turn, multifamily cap rates to also increase, with the consequence that multifamily values plummeted more than 22% off their peak in Q2 2022 as of Q1 2024.

Source: Federal Reserve Bank of St. Louis, Real Capital Analytics (as of 5/2024)

(1) Estimate reflects share of 36-month, floating-rate originations of all 2019-2022 originations reported by Trepp (7.1%) applied to total loan originations from 2019-2022 reported by Yardi ($1.3T) (as of Q2 2024).

The Party is Over

The capital markets dislocation brought on by the Fed’s rate hiking campaign is now contributing to a material issue for multifamily owners.

Nearly $820 billion of multifamily loans are scheduled to mature by year-end 2027 excluding extension options, which options are typically tied to meeting covenants for maximum LTV’s or minimum debt-service coverage ratios. This wall of maturities comes due just as many banks and non-bank debt fund capital markets participants are in retreat, with the number of active multifamily lenders as of 1Q 2024 having reportedly contracted by 55% from its peak in 4Q 2021(2) and remaining lenders tightening standards considerably.

Source: Mortgage Bankers Association (as of Q4 2022)

(2) Newmark Research (as of 4/2024)

The Refinancing Funding Gap

As these multifamily loans mature, many owners face a considerable funding gap. The table next below presents a typical acquisition closed in 2021 with an LTV of approximately 72% at origination. Assuming a 15% decline in property value and no loan amortization, the LTV increases to 85% and achievable loan proceeds under current standards would satisfy only 72% of the existing loan balance, producing a funding gap of 28% of the existing loan balance.

(1) 2021 assumes a 4.25% cap rate and 5.1% loan constant (interest + principal). 2024 assumes 15% cumulative NOI growth, a 5.75% cap rate, and a 7.5% loan constant (interest + principal).

The borrower in this situation faces two choices to avoid default and foreclosure: (i) secure preferred equity or mezzanine debt financing to plug the “refinancing gap” and retain a diluted ownership interest or (ii) sell the property today at a level that satisfies the existing debt despite potentially realizing a loss on their equity investment.

Buyers’ Market for Investors with Liquidity and Conviction

We believe both of these choices facing borrowers with a refinancing funding gap are compelling investment opportunities for well-capitalized multifamily investors to earn outsized returns either through debt, structured equity, or direct equity investment.

The market judgment that currently active multifamily acquirors have is straight forward:

Many sellers in the current market are under pressure to sell or enter into a dilutive recapitalization in order to avoid the adverse consequence of loan foreclosure.

These sellers will likely be forced to capitulate on the valuation of their multifamily properties, meaning that in many cases the active buyer will be able to make a deal at a fully-adjusted cap rate at 5.75% – 6.25% or higher, in any case at a cap rate substantially higher than the 4.25% – 4.75% cap rate the subject property would have commanded as recently as Q1 2022.

At these acquisition cap rates and with government sponsored entity (“GSE”) fixed-rate borrowing costs in the 5.65% – 6.00% range, the yield spread between cap rates and borrowing rates is somewhere between marginally negative to modestly positive.

When the subject multifamily property is, itself, one with significant value-add income growth potential, this yield spread will, on a pro forma basis, become more favorable over the 2-3 year period that the value-add business plan is executed.

In the context of such multifamily value-add property acquisitions, the buyers of these properties are of the judgment that the U.S. economy cannot sustain SOFR at its current high 5.3% level indefinitely and, whether politics or inflation trends dictate, the Federal Reserve will in due course begin to reverse its prior interest rate hike policies.

When this happens, the active buyer today is of the view that cap rates will, in turn, reverse course and snap back directionally toward where they were 18-24 months ago.

Armed with liquidity and this level of conviction, active buyers of value-add multifamily properties today can underwrite value-add acquisitions to total returns in the mid-teens, and higher.

The Naysayer’s Counterpoints

Higher Interest Rates for Longer

While some believe that the Fed will act in 2024 to reverse course on interest rates because inflation has, in fact, come way down from its 9.3% high and is below 3% today, there is a strong body of opinion that inflation remains higher and the economy stronger than the Fed is comfortable with, the implication being that the Fed is far from ready to start dialing back on interest rates. This, in turn, means that we could be in for a much longer period of high interest rates than many felt would be the case at the outset of 2024.

Even if this proves to be the case, today’s active multifamily value-add property buyer does not need the Fed to start cutting in the near term for their investment thesis to work. Rather, these buyers are assuming that the Fed will be forced, for political or other reasons, to act in the 2025-26 timeframe which will result in exit cap rates compressing from current levels within the three to five-year hold periods they contemplate.

If this thesis holds, the mid to high teens total returns that were projected at acquisition remain within reason.

Over Supply of New Multifamily Inventory

While our analysis concludes the need and opportunity for multifamily investment is clear, many investors remain hesitant in general to deploy capital given broad concerns about commercial real estate as an asset class. The pandemic catalyzed various secular shifts impacting real estate, however not all real estate asset classes were impacted equally.

The predominant headline currently underpinning multifamily real estate concerns depressed rent growth amid the wave of new supply being delivered in late 2023 to early 2025. As shown below, quarterly deliveries have been steadily climbing since the beginning of 2022 with trailing-12-month deliveries exceeding 2.0% of inventory in each of the last 4 quarters through 1Q2024 and another 5% of existing inventory scheduled for delivery by the end of 2025.

Source: Axiometrics (as of Q1 2024)

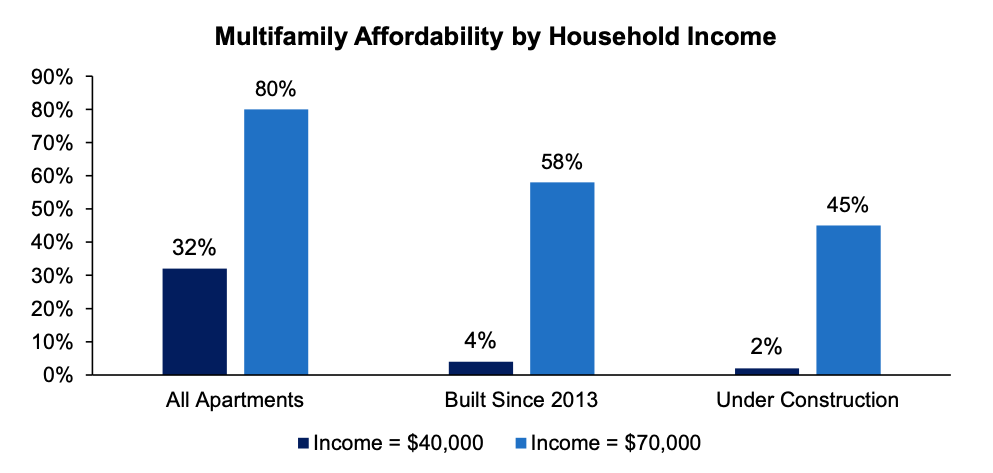

These headline figures are cause for concern, but supply deliveries should be evaluated market-by-market and in the context of location in the sub-market and affordability. Housing is generally considered “affordable” when the renter spends no more than 30% of income on rent plus utilities. For an individual earning $70,000 annually, only 58% of apartments built since 2013 qualify as affordable and only 45% of units under construction are affordable. For blue- and grey-collar workers earning $40,000 annually, the universe of affordable apartments shrinks considerably to include 32% of all apartment units and only 4% of units delivered since 2013. NPRC’s multifamily portfolio weighted average monthly rent of $1,350/month requires a median household income of only $54,000 to meet the “affordable” definition.

Source: CoStar (as of 5/2023); Fannie Mae Multifamily Economic and Market Commentary (as of 2/2020).

The high cost of construction, which continues to rise amid increased public and private infrastructure investments and inflating input costs, requires developers to demand high asking rents for newly built apartment units to achieve their return targets. This means new multifamily construction requires higher-income tenants that can afford the monthly asking rents of $1,800 and higher that developers require to generate the 20%+ returns they seek. This skewed higher rent focus for new construction further insulates existing workforce housing properties, which cater to lower-income demographics, from the extreme rent growth pressures that higher-end luxury multifamily properties are experiencing.

This divergence in rent growth between multifamily asset segments is already emerging. Higher end, Class A properties enjoyed outsized rent growth in 2021 as renters benefited from continued government stimulus and traded up in quality. As markets digested new supply delivered in 2021 and 2022, rent growth trends inverted and lower rent workforce apartments began realizing stronger rent growth. While new supply has reduced overall market rent growth from the 10%+ seen in 2021 and 2022, workforce housing demonstrates a countercyclical resilience with year-over-year rent growth remaining in the range of 3.0% - 5.0% as the broader higher-end rental rate markets approach flat to negative rent growth.

Source: Yardi Matrix (as of Q1 2024)

The Housing Supply and Demand Gap

We believe the long-term need for more naturally-affordable workforce housing persists at a national level despite the substantial inventory under construction. The current pace of building is approximately 247,500 units less per year than demand. This shortfall contributes to the expanding supply and demand gap, estimated at 3.5 million housing units below what is needed.

Source: U.S. Census Bureau (as of 2023), RSM US Research (as of 8/2022)

Meanwhile, restrictive lending conditions, increasing construction costs, and weakening lease-up rent and occupancy fundamentals in over-supplied markets have suppressed new construction starts and permitting. On a trailing-12-month basis, construction starts and permitting has returned to pre-pandemic levels after peaking in late 2022, and deliveries are expected to decline to normalized levels in 2026 and 2027.

Source: Federal Reserve Bank of St. Louis, Real Capital Analytics (as of Q1 2024).

Reinforcing the fact that this supply-demand gap exists, developers are now forced to carry land for longer periods due to the inability to secure financing. The current 500-day average between permitting and construction has increased 45% increase from 2019.

Source: Yardi Matrix (as of Q1 2024).

This trend is anticipated to continue until new supply is absorbed and fundamentals stabilize. As a consequence, the supply-demand balance is expected to revert to historical norms providing support for broad market rent growth following the surge in new supply deliveries through 2025.

Are We Entering the Buying Opportunity of the Century?

Final Thoughts

Many multifamily owners and lenders are contending with considerable headwinds in the current market. Concentrated deliveries and high interest rates make the refinancing of maturing low-interest rate debt next to impossible without the owner writing a check to sufficiently de-leverage the property. Borrowers and lenders have spent the past 18 months utilizing borrower-friendly “amend and extend” strategies in an effort to wait out the refinancing dilemma. In our view, this party appears to be over, and lenders are now demanding that borrowers write the de-leveraging check in order to buy another maturity extension.

We believe these near-term capitalization problems for some multifamily owners create the investment opportunity for multifamily investors armed with liquidity and conviction that valuations will directionally snap back toward cap rates that existed before the Fed’s rate-hiking campaign started in Q2 2022.

In this regard, for the reasons cited herein, NPRC has the view that this valuation opportunity is most clearly in the suburban, garden-style, older vintage, market rate, naturally affordable, value-add workforce housing segment of the multifamily real estate market.

DISCLOSURES

Not an Offer or Solicitation: This is for informational purposes only and is not an offer or solicitation to purchase or sell any financial instrument or service to any person in any jurisdiction. This is not intended to be construed as investment advice, an investment recommendation, investment research, or a recommendation about the suitability or appropriateness of any security, commodity, investment, or particular investment strategy. Reliance upon this information is at the sole discretion of the listener and the listener should consider the investment objectives, risks, charges, and expenses of any investment carefully before making it. This is intended to be shared as National Property REIT Corp. (“NPRC” or “We”) brand awareness and illustrate NPRC’s role in owning and operating real estate in the market segments discussed herein.

Unless otherwise mentioned, the views, opinions and/or beliefs contained herein are those of NPRC employees. Other past or present NPRC employees, or other past or present employees of NPRC’s affiliates, may not necessarily share the same views, opinions and/or beliefs of present NPRC employees, and may not make, or may not have made, the same decisions regarding the ownership, operation and financing of real estate in the market segments discussed in herein. These views, opinions, beliefs, estimates and projections are made in relation to the facts known at the time of preparation and are subject to change at any time without notice. DO NOT RELY ON ANY OPINIONS, BELIEFS, PREDICTIONS OR FORWARD-LOOKING STATEMENTS CONTAINED HEREIN. Certain statements made throughout this information may be “forward-looking” in nature. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. There can be no assurance that any trends discussed during this presentation will continue and neither NPRC nor any of its affiliates has any responsibility to update this presentation to account for such changes. Certain information contained herein may have been obtained from third party sources. Although NPRC believes such sources to be reliable, NPRC makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties.

A number of factors may prevent each of NPRC’s properties from generating sufficient net cash flow or may adversely affect their value, or both. These factors include, but are not limited to, national economic conditions, regional and local economic conditions (which may be adversely impacted by plant closings, business layoffs, industry slow-downs, weather conditions, natural disasters, and other factors), local real estate conditions (such as over-supply of or insufficient demand), changing demographics, perceptions by prospective tenants of the convenience, services, safety, and attractiveness of a property, the ability of property managers to provide capable management and adequate maintenance, the quality of a property’s construction and design, increases in costs of maintenance, insurance, and operations (including energy costs and real estate taxes), changes in applicable laws or regulations (including tax laws, zoning laws, or building codes), potential environmental and other legal liabilities, the level of financing used by NPRC in respect of its properties, increases in interest rate levels on such financings and the risk that NPRC will default on such financings, each of which increases the risk of loss, the availability and cost of refinancing, the ability to find suitable tenants for a property and to replace any departing tenants with new tenants, potential instability, default or bankruptcy of tenants in the properties owned by NPRC, potential limited number of prospective buyers interested in purchasing a property that NPRC wishes to sell, and the relative illiquidity of real estate investments in general, which may make it difficult to sell a property at an attractive price or within a reasonable time frame.

The distribution of this information is restricted by law. No action has been or will be taken by NPRC to permit the possession or distribution of this information in any jurisdiction, where action for that purpose may be required. Accordingly, this information may not be used in any jurisdiction except under circumstances that will result in compliance with all applicable laws and regulations.